State of Proptech Venture Capital: June 2026

In June 2026, proptech companies raised $650.4 million across 30 announced financings, based on disclosed funding rounds.

The month was defined by a handful of large financings. Nesto, Higharc, Square Yards, Endra, and Enex collectively accounted for more than three-quarters of all disclosed capital raised. While residential technology attracted the largest share of investment, construction and development recorded one of their strongest months of the year, reflecting continued investor conviction in technologies supporting the planning, design, construction, and modernization of the built environment.

Rather than concentrating capital around a single theme, June's funding activity spanned the real estate lifecycle—from mortgage and residential operations to AI-powered engineering, homebuilding, energy systems, and commercial real estate property technology.

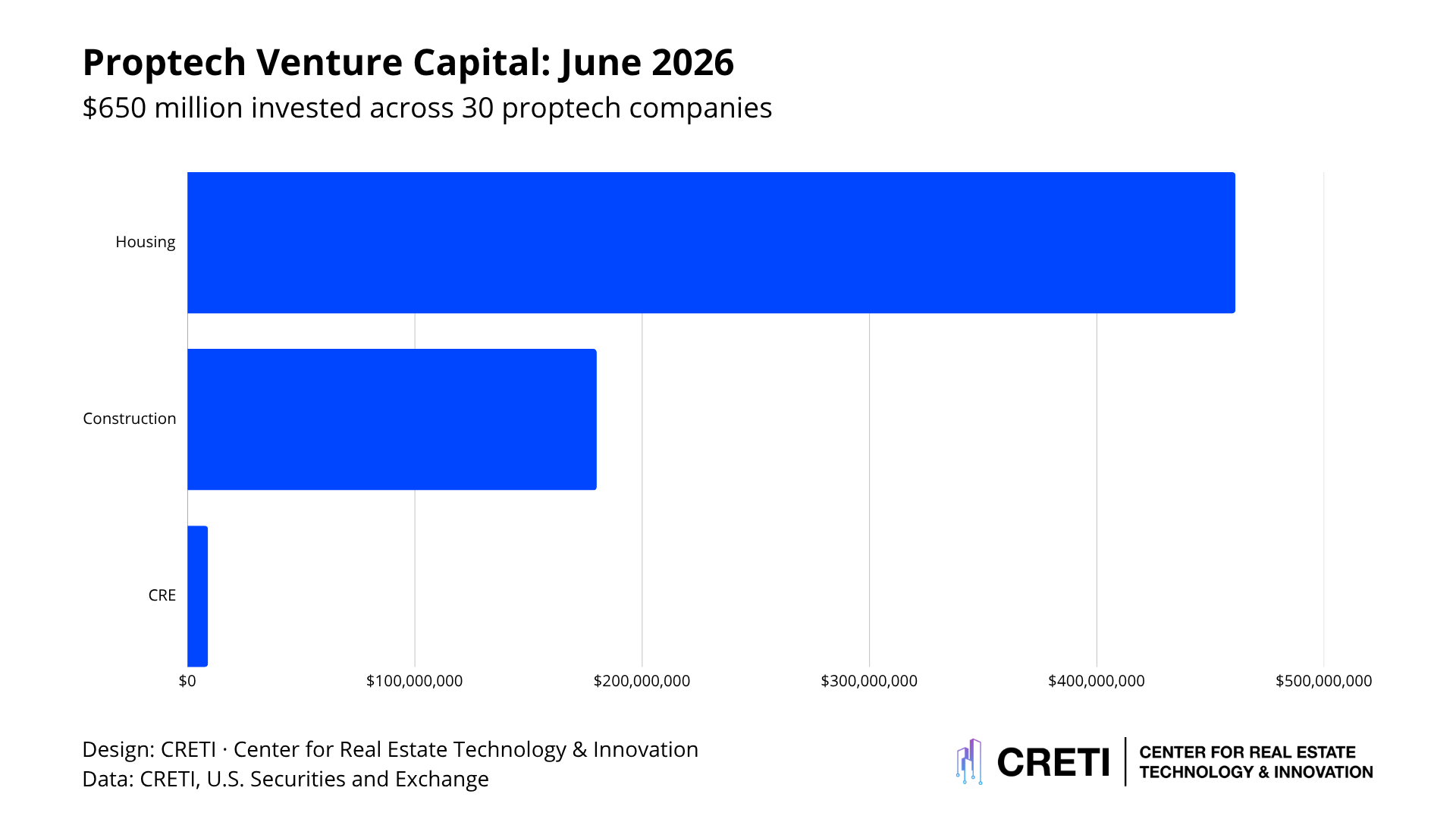

Housing: $461.0 Million (70.9%)

Housing remained the largest destination for venture capital during June.

The largest financings included Nesto ($216.5M), Square Yards ($95M), and Findigs ($32M).

Additional capital flowed into residential operations, community management, affordable housing, rental technology, property intelligence, and homeownership platforms through companies including MyGate, MW, Lhoopa, Agenz, Zazume, Propsoch, Return Valets, Joymee, and BrokerPlus.

The concentration reflects the continued attractiveness of residential real estate to venture investors. Housing combines transaction frequency, fragmented ownership, recurring consumer demand, financing, brokerage, maintenance, and property operations. The total addressable market is substantial: U.S. residential real estate represents approximately $50 trillion in asset value, while multifamily alone accounts for roughly $4 trillion.

Construction & Development: $179.6 Million (27.6%)

Construction and development represented the second-largest category by capital deployed during June.

The largest financings included Higharc ($95M), Endra ($50M), and Aston Power ($20M).

Additional funding supported AI-powered engineering, construction compliance, building inspection, sustainable materials, and construction automation through companies including H3 Zoom.AI, Circular 11, Kestrel Labs, and Simply Agnostic.

The allocation reflects continued investor interest in technologies that improve how buildings are designed, engineered, permitted, and delivered. Capital continues to concentrate around measurable productivity gains in preconstruction, design automation, engineering workflows, and building infrastructure rather than broad construction software platforms.

CRE & Building Operations: $9.0 Million (1.4%)

Commercial real estate and building operations accounted for a comparatively small share of June funding.

The largest financings included Subbase ($7M), reltix ($3.45M), and CentralComs ($500K).

Capital was directed toward property management, maintenance automation, operational workflows, and asset management systems rather than transaction platforms.

The allocation reflects the current commercial real estate environment. Owners continue prioritizing technologies that improve operational efficiency, automate repetitive workflows, and enhance asset performance rather than platforms tied primarily to leasing velocity or acquisitions.

What This Means for Proptech

June's funding activity reinforces two themes that have become increasingly evident throughout 2026.

First, housing continues to attract the largest pools of capital because it remains the most active and economically significant segment of real estate. Investors continue backing platforms that improve mortgage origination, residential transactions, community operations, and property management.

Second, construction technology continues to mature into one of proptech's largest investment categories. Higharc's $95 million financing and Endra's $50 million Series A illustrate growing investor conviction in AI-enabled design, engineering automation, and technologies that improve how buildings are planned and delivered.

Commercial real estate funding remained comparatively modest and concentrated around property operations rather than transaction activity. The allocation suggests investors continue prioritizing operational performance, workflow automation, and asset efficiency over expansion-oriented platforms.

Taken together, June's funding activity reflects a market that is becoming increasingly disciplined in how capital is deployed. Investors continue directing larger pools of capital toward technologies embedded directly within the economics of real estate—whether through housing finance, construction productivity, or operational performance—while reserving the largest rounds for companies that have demonstrated scale and commercial traction.