Proptech Venture Capital by Funding Stage: May 2026

In May 2026, proptech companies raised $353 million across 39 deals, with a median funding round of $11 million. While total funding remained healthy, the more revealing story lies in how capital was distributed across funding stages.

The month's activity highlights a venture market that continues to support companies throughout the growth lifecycle, but with a clear preference for businesses that have already demonstrated traction. Larger rounds accounted for the majority of capital deployed, while early-stage activity remained active in terms of deal count but represented a smaller share of total dollars invested.

The distribution of capital suggests investors remain willing to fund innovation across proptech, but are increasingly concentrating larger checks into companies with proven products, established customers, and clearer paths to scale.

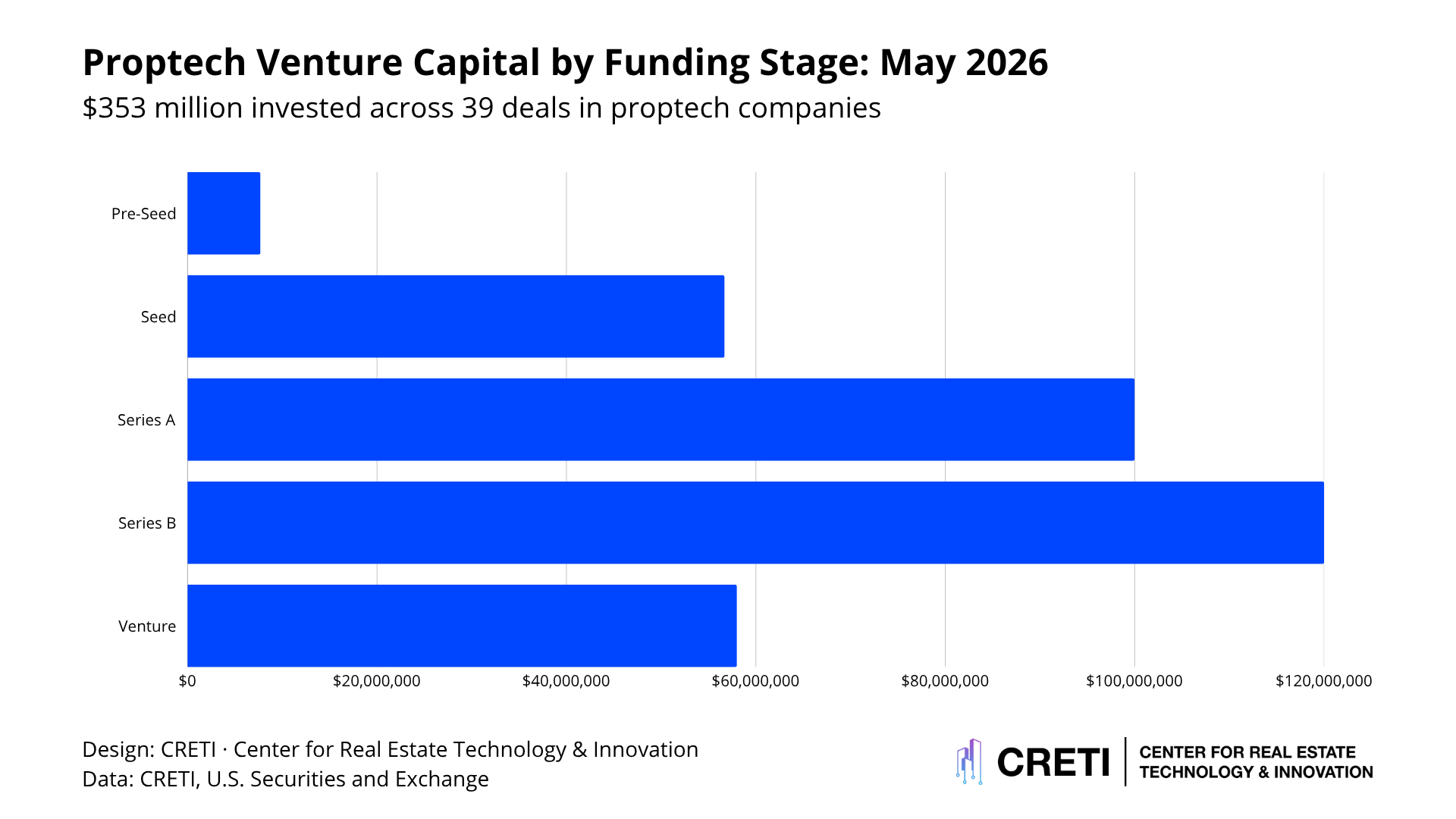

Pre-Seed: $7.7M

Pre-seed companies raised approximately $7.7 million, representing 2.6% of disclosed capital during May.

The largest rounds included Davis AI ($5.5M), ENVIOTECH ($1.2M), and Layn ($1.0M).

These financings were directed toward founders validating new concepts across construction technology, sustainability infrastructure, AI workflows, and operational systems.

While pre-seed represented the smallest share of capital deployed, it remains an important indicator of where future innovation may emerge across the built environment.

Seed: $56.7M

Seed-stage companies raised $56.7 million, accounting for 18.9% of disclosed capital during the month.

The largest Seed financings included Drafted ($16M), Balcony ($12.7M), and ProcurePro ($11M).

Seed activity remained broad, spanning construction technology, financial infrastructure, property operations, housing platforms, and AI-enabled workflow automation. Investors continued to back companies that have moved beyond concept validation and are beginning to demonstrate repeatable customer adoption.

The level of activity at the Seed stage suggests venture firms remain committed to funding the next generation of category leaders, even as the broader market becomes more selective.

Series A: $100.2M

Series A represented the largest funding category during May, accounting for 33.3% of disclosed capital.

The category was led by Fifth Dimension AI ($26M), LightTable ($22M), and Cedar ($22.2M).

Series A companies typically occupy a critical phase within the venture lifecycle. Product-market fit has often been established, customer adoption is accelerating, and capital is being deployed to scale teams, expand distribution, and deepen product capabilities.

The concentration of funding at this stage reflects continued investor confidence in companies that have demonstrated early traction but still have substantial room for growth.

Series B: $120.1M

Series B companies attracted $120.1 million, making it the largest funding stage by capital deployed during May.

The largest financings included Smartness ($55.1M), Handle ($27M), and Pronto ($20M).

Series B companies are typically transitioning from product-market fit toward operational scale. Capital is often used to accelerate customer acquisition, expand into new markets, strengthen leadership teams, and support broader organizational growth.

The strength of Series B activity suggests investors continue supporting companies that have successfully navigated early-stage growth and are positioned to become leaders within their respective categories.

Venture: $58.2M

Venture financings accounted for $58.2 million of disclosed capital during May.

The largest rounds included Smartness ($55.1M) and Terra CO2 Technologies ($22M). Additional funding flowed into companies focused on construction materials, sustainability infrastructure, project execution, and operational technology.

The category represents companies that have progressed beyond traditional venture stages but are not necessarily raising institutional Series C or later rounds. These financings are often tied to expansion, commercialization, and scaling efforts rather than product validation.

The concentration of capital within a handful of larger venture rounds highlights continued investor appetite for businesses addressing large operational and infrastructure challenges across the built environment.

What This Means for Proptech

May's funding activity highlights a venture market that remains active across all stages of company development, but increasingly favors businesses that have moved beyond experimentation and into execution.

Series A and Series B companies accounted for the majority of disclosed capital deployed during the month. Investors directed funding toward businesses that have demonstrated customer adoption, operational maturity, and a clear path toward scale.

Seed activity remained healthy, reflecting continued support for emerging companies across construction, housing, finance, and real estate operations. Pre-seed investment also remained active, though capital deployment at the earliest stages was modest relative to later-stage financings.