State of Proptech Venture Capital: May 2026

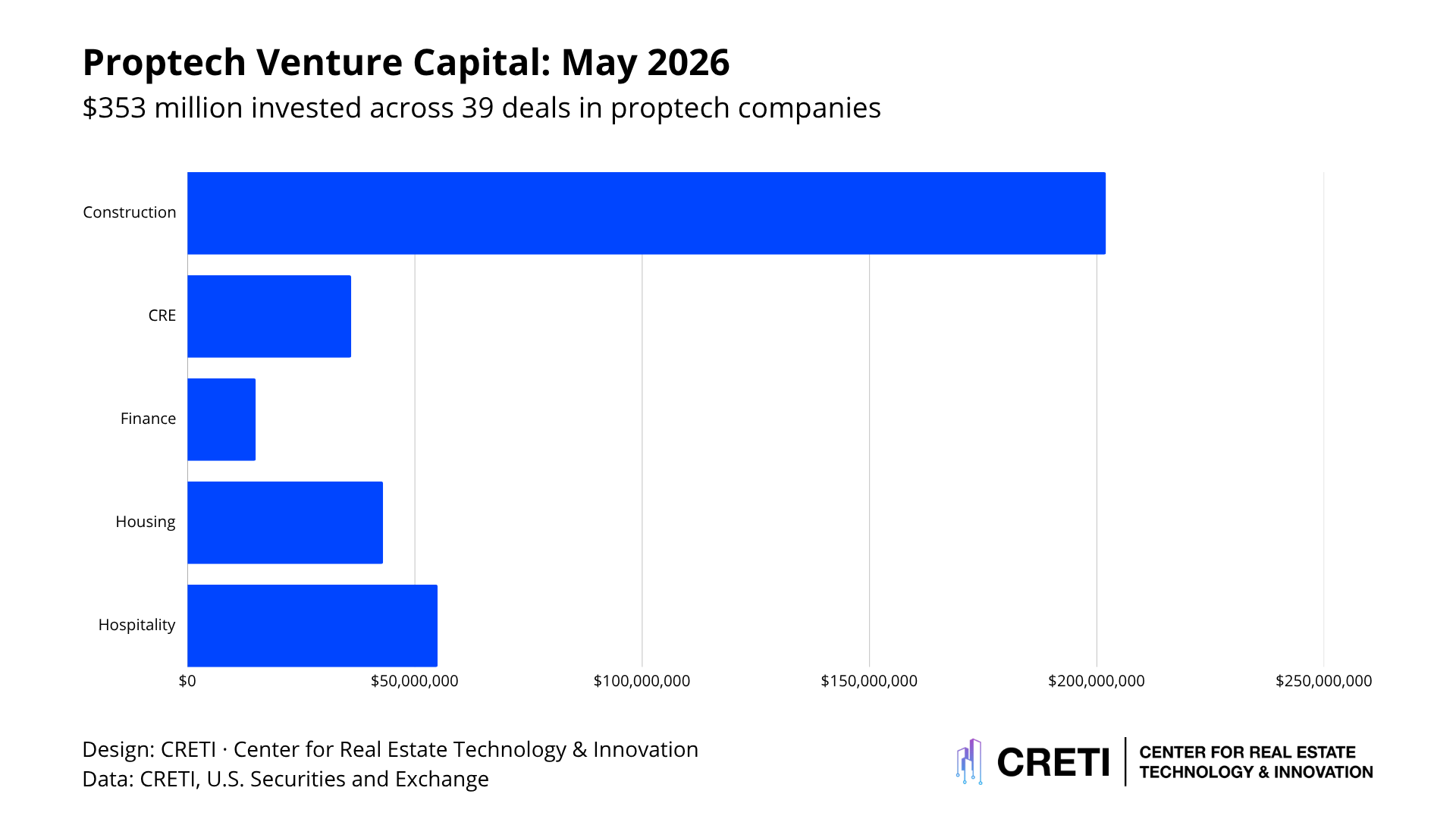

In May 2026, proptech companies raised $353.0 million across 39 deals, with a median funding round of $11 million. On the surface, the numbers point to one of the more active funding months of the year. Beneath the headline, the allocation of capital shows a market that remains highly selective in where it is willing to underwrite growth.

Construction and development captured the majority of capital deployed during the month, supported by investor appetite for technologies tied to project execution, procurement, materials, automation, and construction finance. Hospitality also accounted for a meaningful share of funding, driven by a single large round in a revenue management platform. Housing remained active but less dominant than in April, while commercial real estate funding continued to concentrate around asset intelligence and operational systems rather than transaction-led platforms.

Construction & Development: $202.8M, 57.4%

Construction and development was the largest category by a wide margin, accounting for $202.8 million, or 57.4% of total capital deployed in May.

The largest rounds included Xpanner ($36.0M), Handle ($27.0M), and Cedar ($22.2M).

The breadth of funding across the category is notable. Capital was not concentrated in one narrow part of the construction stack. It moved across procurement, construction finance, AI-enabled design and coordination, low-carbon materials, project execution, workforce systems, and modular or industrialized building processes.

The allocation reflects continued investor interest in one of real estate’s most persistent problems — the difficulty of building efficiently. Construction remains fragmented, labor-intensive, and exposed to cost volatility. Investors appear to be funding platforms that can address specific operational failures rather than companies promising to digitize the entire construction lifecycle.

Hospitality: $55.1M, 15.6%

Hospitality accounted for $55.1 million, or 15.6% of total May funding.

The category was led by Smartness ($55.1M), which represented the largest hospitality-related financing of the month. The company’s focus on pricing and revenue management reflects continued demand for technology that can improve yield, occupancy, and operating performance across hotels and short-term rental portfolios.

Hospitality remains a smaller category within proptech compared with housing or construction, but May’s data shows that investors remain willing to back platforms tied directly to revenue optimization. In a sector where margins are sensitive to occupancy, pricing, labor, and seasonality, software that improves revenue decision-making can command institutional interest.

Housing: $43.5M, 12.3%

Housing accounted for $43.5 million, or 12.3% of total capital deployed during May.

The largest housing-related financings included Pronto ($40.0M), alongside smaller rounds for Jinka, eVoost AI, VillaFact, Driive, and Landovo. The category included platforms tied to home services, housing search, residential transactions, and digital ownership or service infrastructure.

Housing remained active, but it was not the dominant capital destination in May. That contrasts with April, when residential and multifamily platforms accounted for the majority of funding. The category continues to benefit from transaction frequency, fragmented ownership, recurring consumer demand, and multiple monetization layers across financing, brokerage, maintenance, and services.

The TAM remains considerable. U.S. residential real estate is roughly a $50 trillion asset class, while multifamily alone is approximately $4 trillion. Even in months when housing does not lead capital allocation, it remains one of the most durable areas of proptech because of its scale and recurring demand characteristics.

CRE & Building Operations: $36.5M, 10.3%

Commercial real estate and building operations accounted for $36.5 million, or 10.3% of total funding.

The category was led by Fifth Dimension AI ($26.0M), followed by ChampAI ($8.5M) and Pluria ($2.0M). Funding was directed toward decision intelligence, workflow automation, workplace access, and operational systems rather than leasing marketplaces or transaction acceleration platforms.

The capital flowing into CRE was primarily tied to performance, utilization, and operating efficiency. That fits the current market environment. Owners and investors remain focused on improving the performance of existing assets, understanding portfolio risk, and reducing manual workflows across asset management and operations.

This was not a month in which CRE capital chased expansion. It focused on systems that help owners make better decisions and run assets more efficiently.

Real Estate Finance: $15.2M, 4.3%

Real estate finance accounted for $15.2 million, or 4.3% of total funding.

The category included Balcony ($12.7M) and Paydas ($2.5M). These platforms sit closer to payments, property records, investment access, and transaction infrastructure than to traditional operating software.

The category was smaller than construction, hospitality, and housing, but it remains strategically important. Financial infrastructure often offers some of the clearest monetization opportunities in proptech because it participates directly in how money, ownership, records, and investment flow through real estate.

Even when it does not command the largest share of capital, it remains one of the more investable areas of the market because revenue models can be tied directly to transactions, fees, or capital movement.

What This Means for Proptech

May’s funding activity showed a market that was active but not indiscriminate. Capital was concentrated in areas where investors could see a clearer connection between technology and economic performance.

“Venture investors are still deploying, but continue to be selective, said Jenny Song, Partner at Navitas Capital. “We're seeing a higher bar for revenue traction, moats, and total market opportunity, especially in software start-ups.”

Construction led the month because the sector still contains some of the largest productivity gaps in the built environment. Investors directed funding toward platforms that address project execution, procurement, materials, automation, and construction finance. The emphasis was not on broad platform narratives, but on specific points of operational leverage.

Hospitality’s share was driven by a large revenue management financing, reinforcing that investors remain interested in categories where software can improve pricing, yield, and operating performance. Housing activity remained active but at a lower share than the prior month, suggesting that capital is rotating across the real estate lifecycle rather than concentrating solely in residential platforms.

CRE and building operations continued to attract capital where platforms improve asset intelligence, utilization, and workflow automation. Financial infrastructure remained smaller in dollar terms but remained relevant because it sits close to the movement of money and ownership in real estate.

"May's funding data shows that investors remain active in proptech, but increasingly disciplined," said Ashkan Zandieh, Founder and Managing Director of CRETI. "Capital is flowing toward technologies that can be directly connected to productivity gains, revenue growth, asset performance, and capital efficiency. The market is rewarding solutions that address measurable business outcomes."