State of Proptech Venture Capital: April 2026

In April 2026, proptech companies raised $325 million across 42 deals, with a median funding round of $3.9 million. On the surface, the numbers suggest a relatively healthy venture environment. Beneath the surface, however, the allocation of capital tells a more revealing story about where investors believe value in real estate technology will actually accrue over the next several years.

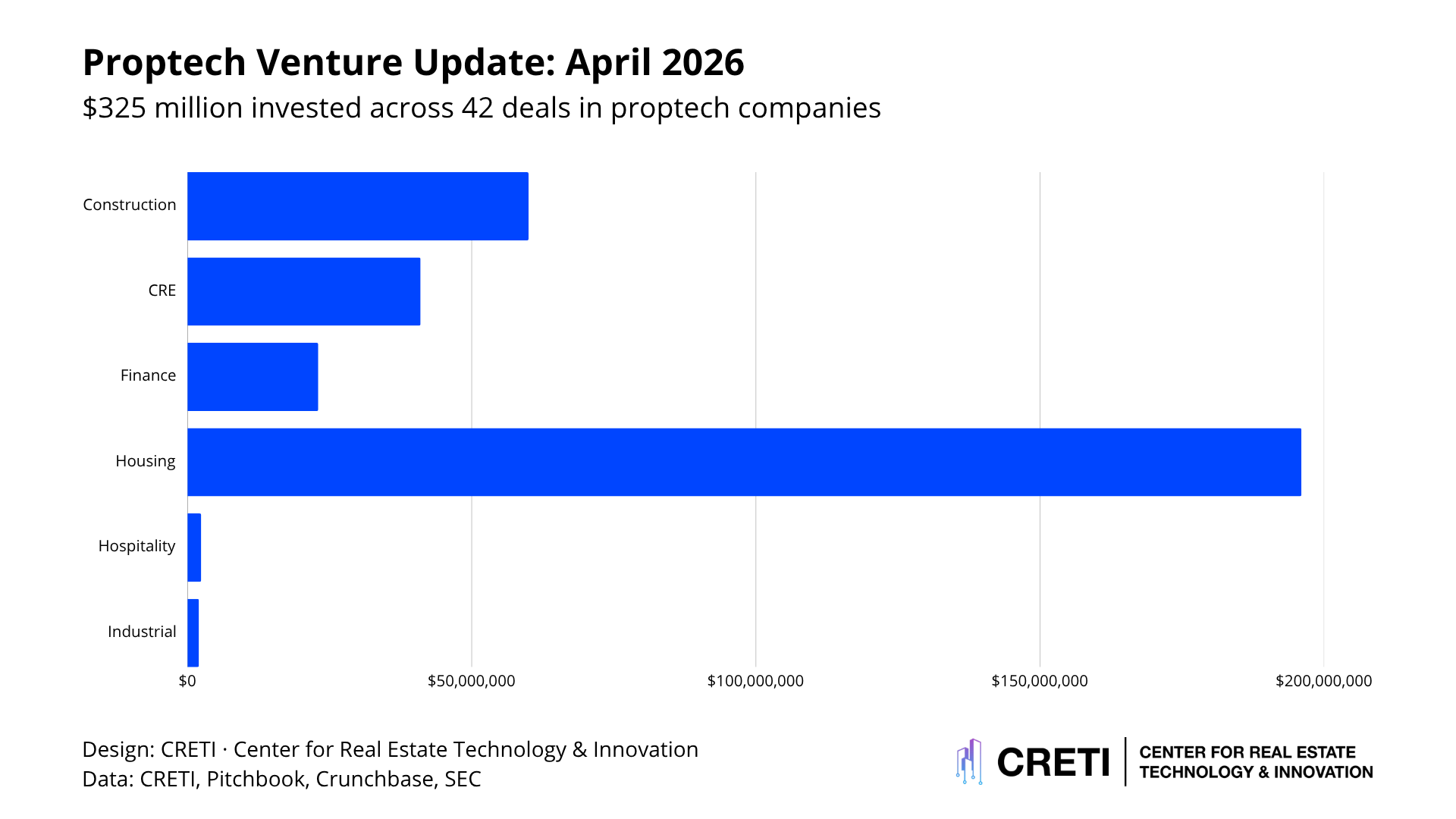

Housing dominated investment activity in April, while commercial real estate funding remained comparatively restrained and highly selective. Construction technology continued attracting targeted capital, though primarily around workflow efficiency and procurement rather than broad platform expansion.

Housing: $196.6M, 60.4%

Housing, a combination of residential and multifamily, was the largest category by a wide margin. The largest rounds included Snabbit at $56M, Habi at $40M, HomeLight at $40M, True Footage at $40M, and Casavo at $14.1M.

The concentration reflects the continued attractiveness of residential real estate to venture investors. Housing combines transaction frequency, fragmented ownership, recurring consumer demand, and multiple monetization layers across financing, brokerage, maintenance, and services. The TAM is also enormous: U.S. residential real estate is roughly a $50T asset class, while multifamily alone is approximately $4T.

Construction & Development: $60.1M, 18.5%

Construction was the second-largest category after moving All3 into construction. The category included All3 at $25M, Primepoint at $10M, People & Technology at $9.9M, CONXAI at $5.8M, Azure Printed Homes at $3.9M, Onestruction at $3.0M, and Traza at $2.1M.

Construction funding remains focused on execution, workflow automation, procurement, materials, and AI-enabled project intelligence. The category is gaining share, but capital is still being deployed into specific operational bottlenecks rather than broad construction platforms.

CRE & Building Operations: $41.2M, 12.7%

Commercial Real Estate and building operations accounted for $41.2M. Mappedin led the category at $24.5M, followed by Loki Robotics at $11.8M, HELIXintel at $3M, Kairos at $1.6M, and Vuabl at $294K.

The capital flowing into CRE was not primarily tied to transactions. It was directed toward mapping, building operations, maintenance, robotics, and asset visibility. That fits the current CRE environment, where owners are focused less on expansion and more on improving the performance of existing assets.

Financial Infrastructure: $23.0M, 7.1%

Financial infrastructure included Fence at $20M and Truss at $3M. These platforms sit close to payments, financing, and transaction execution.

This category remains important because it captures value from how money moves through real estate. Even when it is not the largest allocation, it often represents some of the clearest monetization in proptech.

Hospitality: $2.4M, 0.7%

Hospitality remained small, led by Otel AI at $2.4M. The category is still active, but April’s data shows limited disclosed capital compared with housing and construction.

Industrial & Infrastructure: $2.0M, 0.6%

Rebound Technologies accounted for $2.0M. This category remains highly specific, tied to industrial systems, cooling, energy efficiency, and physical infrastructure.

What This Means for Proptech

April’s funding activity reinforces a broader shift underway across proptech investing: capital is increasingly flowing toward platforms positioned closest to the economic engine of the asset itself.

Housing attracted the majority of investment because it remains the most transaction-oriented and consumer-participatory segment of real estate. Commercial real estate funding concentrated around operational visibility because owners are prioritizing asset performance over expansion. Construction technology continued attracting selective capital where efficiency gains can be measured clearly and operationally.

The result is a market becoming more operational, more economically grounded, and more disciplined in how technology is underwritten.

Investors are still funding real estate technology. But increasingly, they are funding technologies tied directly to transaction activity, operating performance, utilization, procurement, and capital flow.

That distinction is increasingly defining the current phase of the proptech market.Construction and Development