Proptech Venture Capital in Q1 2026: Growth in Capital, Increasing Concentration

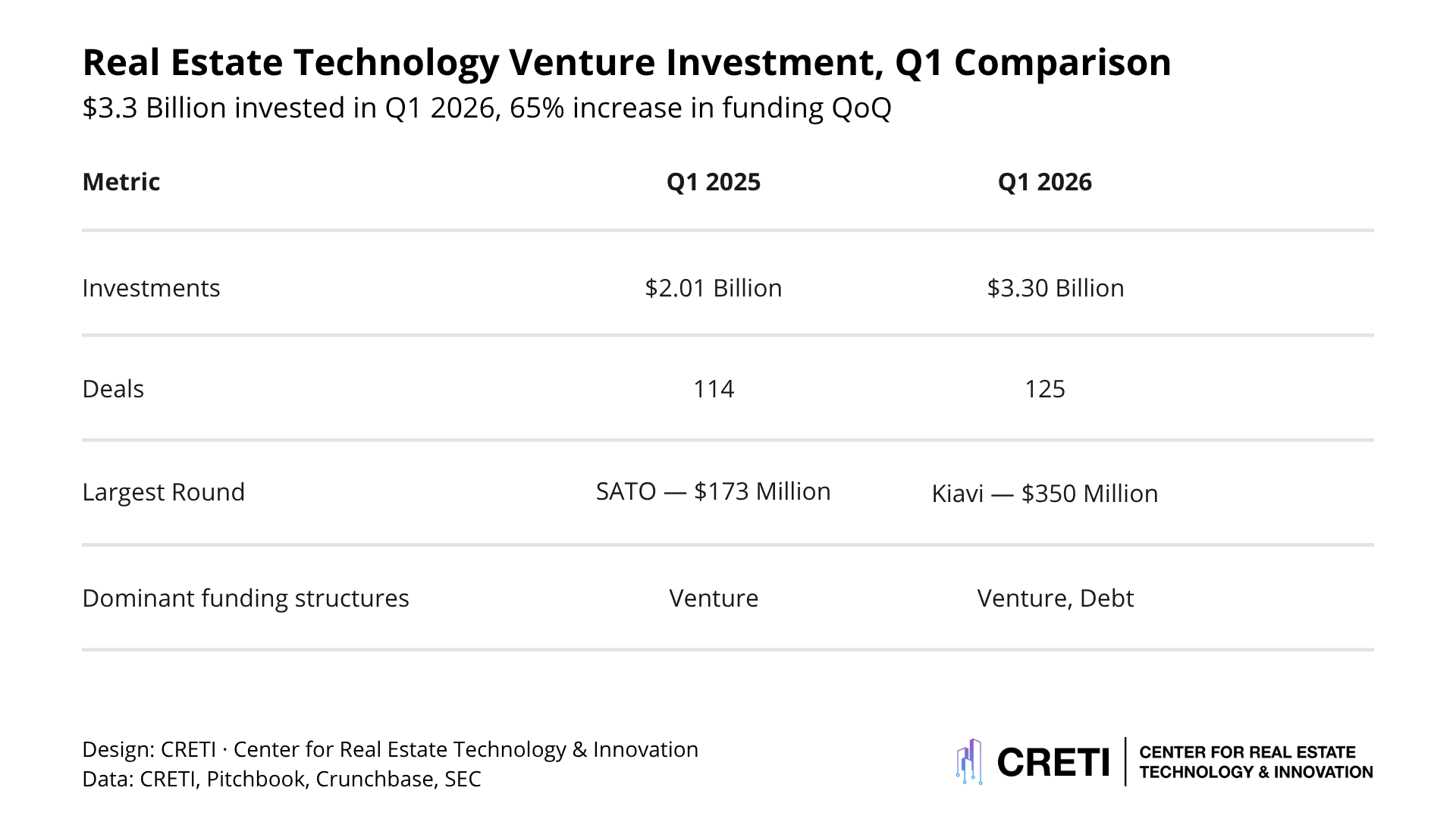

Proptech investment activity strengthened in Q1 2026, with total funding reaching $3.30 billion across 125 transactions, compared with $2.01 billion across 114 transactions in Q1 2025. Despite this increase in deployed capital, the median deal size declined slightly to $8.0 million from $8.4 million, suggesting that pricing did not expand across the broader market.

Instead, the quarter was characterized by a concentration of capital in a limited number of large financings, alongside continued activity at the early stage. This combination reflects a proptech-venture market that is expanding in aggregate terms while becoming more selective in capital allocation.

Three dynamics define the quarter:

A disproportionate share of capital concentrated in large transactions

Continued discipline in early-stage and mid-stage pricing

An expanding role for non-venture capital structures, including debt and private equity

Collectively, these trends suggest that proptech is evolving toward a more mature and differentiated capital market structure.

Capital Growth Was Driven by Large Transactions

While total investment increased materially year over year, capital deployment was not evenly distributed.

The top 10 transactions accounted for approximately $2.03 billion, representing roughly 62 percent of total capital deployed in Q1 2026. This level of concentration indicates that aggregate growth was driven by a relatively small set of large financings rather than broad-based increases in deal size.

The largest transactions in the quarter included:

Kiavi — $350 million (Debt)

Mews — $300 million (Series D)

Convene — $230 million (Debt)

Terralayr — $223.2 million (Venture)

Terralayr — $189.7 million (Debt)

Property Finder — $170 million (Private Equity)

Span — $163.3 million (Venture / Corporate)

Weaver Services — $156.1 million (Venture)

Roc360 — $150 million (Private Equity)

Propy — $100 million (Debt)

These transactions were concentrated in companies operating across housing finance, energy systems, transaction infrastructure, and large-scale operational platforms. Many of these businesses exhibit characteristics more commonly associated with infrastructure or financial services than traditional venture-backed software.

Excluding these large transactions, the remainder of the market aligns more closely with the observed median deal size, reinforcing the view that capital remains disciplined outside the upper tier of financings.

The Capital Stack Continued to Diversify

Q1 2026 saw a continued expansion in the types of capital deployed.

Debt accounted for approximately one-third of total capital, with private equity contributing an additional meaningful share. Combined, these sources represented close to half of all capital invested.

This reflects a shift toward a more layered capital stack, including:

Venture capital for early-stage innovation

Growth equity for scaling platforms

Debt for asset-backed or revenue-generating businesses

Private equity for more mature operating models

The presence of debt across multiple large transactions suggests that certain proptech companies—particularly those tied to lending, infrastructure, or transaction flows—are increasingly able to support non-dilutive capital structures.

Early-Stage Activity Remained Broad but Disciplined

Early-stage investment remained a significant component of the market.

Q1 2026 included 52 seed and pre-seed transactions, accounting for approximately 42 percent of total deal volume, but only about 4 percent of total capital deployed.

The largest seed financings of the quarter included:

Zero RFI — $13.8 million

Krane — $9.0 million

Smart Bricks — $5.0 million

Sitegeist — $4.7 million

EstateXchange — $8.4 million

These companies span construction automation, AI workflows, property infrastructure, and marketplace platforms.

While innovation remains broad, capital deployment at this stage remains measured, suggesting that investors are maintaining discipline in entry pricing and check size.

Series A Activity Reflects Selective Scaling

Series A rounds remained active, though selective.

Q1 2026 included 12 Series A transactions, supporting companies transitioning from early traction to scaled growth.

The largest Series A rounds included:

Metiundo — $47.6 million

Zero Homes — $16.8 million

Rebar — $14.0 million

Foresight Works — $25.0 million

Trayd — $10.0 million

These companies are primarily focused on energy systems, housing platforms, construction workflows, and operational infrastructure.

Across Series A, investors appear to be prioritizing companies that demonstrate clear paths to revenue scale and operational impact, rather than funding based solely on growth potential.

Comparison to Q1 2025

The comparison with Q1 2025 highlights a structural shift.

Q1 2025 was characterized by:

Lower total capital

Slightly higher median deal size

More evenly distributed capital across transactions

In contrast, Q1 2026 shows:

Higher aggregate capital deployment

Lower median deal size

Increased concentration of capital in large transactions

Greater participation from debt and private equity

These differences suggest that capital has returned to the sector, but is being deployed in a more targeted and selective manner.

Sector-Level Implications

The largest financings provide insight into where investors are concentrating capital.

Funding in Q1 2026 was disproportionately allocated to sectors tied to:

Financial infrastructure and lending

Energy and electrification systems

Transaction platforms and marketplaces

Large-scale operational systems

These sectors tend to offer stronger revenue visibility and scalability.

In contrast, traditional proptech categories—particularly workflow software—continue to attract investment primarily at earlier stages and smaller round sizes.

Implications for Investors

Several conclusions emerge from Q1 2026 activity.

First, the increase in capital reflects concentration rather than broad expansion.

Second, the growing role of debt and private equity indicates that proptech is increasingly intersecting with capital markets and infrastructure investing.

Third, early-stage activity remains strong, but capital deployment is disciplined, reinforcing the importance of selectivity at entry.

What This Mean for Proptech

Q1 2026 reflects a proptech market that is growing in aggregate capital while becoming more structured in how that capital is deployed.

Large financings are concentrated in companies operating at scale across financial and infrastructure systems, while early-stage innovation continues under disciplined conditions.

This pattern suggests a sector moving toward greater maturity, where capital allocation is increasingly differentiated by stage, business model, and alignment with underlying real estate economics.