State of Proptech Venture Capital: February 2026

Real estate technology investment remained active during the first two months of 2026, though venture capital deployment showed signs of increased selectivity between January and February.

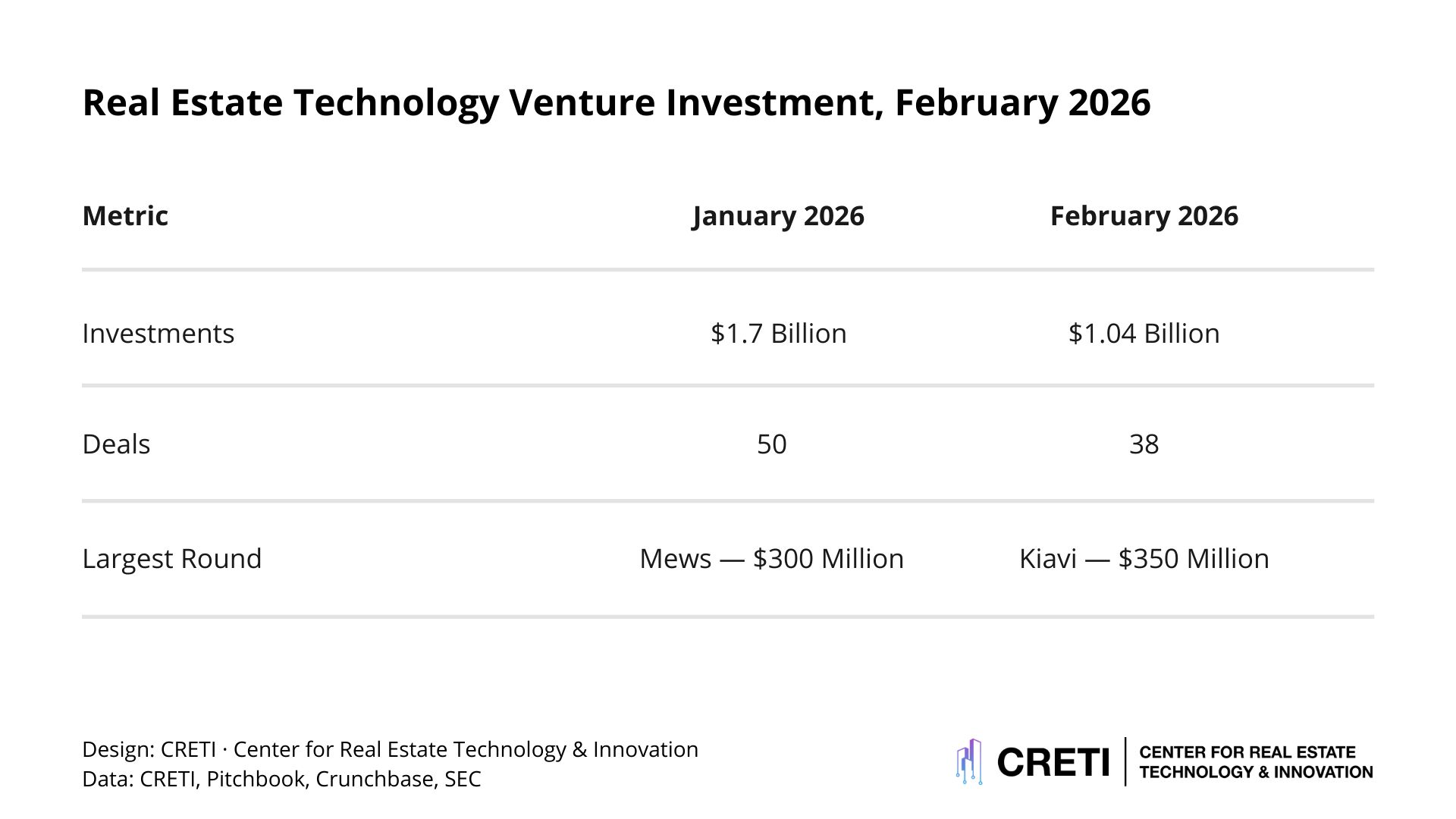

In February 2026, companies across the proptech ecosystem raised approximately $1.04 billion across 38 transactions, with a median deal size of $6.6 million, according to CRETI research.

While January saw broader participation across venture markets, February’s data suggests a more concentrated funding environment characterized by fewer transactions and a greater share of capital allocated to a small number of large financings.

This dynamic reflects a venture capital environment in which investors continue to support early-stage innovation while directing larger capital allocations toward companies operating at scale across infrastructure systems, financial networks, and real estate transaction platforms.

February 2026 Investment Snapshot

Although the number of transactions declined relative to broader venture activity observed earlier in the year, the presence of several large financings materially influenced total capital deployed.

Fewer Transactions Suggest Increasing Venture Discipline

A key difference between January and February lies in the number of financings completed across the sector.

January venture activity included a wider set of early-stage financings and experimental startup formations. By February, however, deal flow had narrowed, resulting in a smaller number of total transactions.

This pattern is consistent with broader venture capital market dynamics in which investors increasingly focus on companies demonstrating measurable traction, revenue visibility, and operational scalability.

While startup formation continues, venture capital firms appear to be applying more rigorous underwriting standards when deploying new capital.

Large Growth Rounds Influenced February’s Capital Totals

Several large transactions played an outsized role in shaping February’s funding totals.

Among the largest financings were:

Kiavi, $350 Million, Debt

Dwelly, $50 Million, Debt

Metiundo, $47.6 Million, Series A

OneDome, $34.2 Million, Series C

Stake, $31 Million, Series B

Ownwell, $30 Million, Series B

Orchard, $30 Million, Venture

These transactions alone accounted for a significant portion of total capital deployed during the month.

When these largest rounds are excluded from the dataset, the distribution of deal sizes more closely reflects the $6.6 million median, indicating that most venture financings occurred at typical early-stage levels.

Early-Stage Formation Continues

Although the number of deals declined relative to January activity, early-stage venture formation remained active in February.

Pre-seed and seed rounds accounted for a meaningful share of the 38 transactions observed during the month.

These startups were distributed across North America, Europe, the Middle East, and Asia, reflecting the continued globalization of proptech innovation.

Many early-stage companies focused on areas including:

Construction technology

AI-enabled operational software

compliance and regulatory platforms

Property transaction infrastructure

Raise sizes at this stage generally fell below the monthly median, reflecting typical early-stage venture financing dynamics.

Financial and Infrastructure Platforms Attract Larger Capital

The largest financings observed in February were concentrated in companies operating at the intersection of real estate and adjacent sectors such as energy infrastructure, financial technology, and transaction platforms.

Companies in these categories often operate across large networks of properties or financial transactions, allowing them to scale more rapidly than narrowly focused workflow software products.

As a result, investors appear increasingly willing to deploy larger amounts of capital into businesses capable of supporting infrastructure-level platforms across the built environment.

This trend reflects a broader shift in venture capital strategy across proptech, where investors are prioritizing companies that can reshape operating models across property markets rather than simply digitizing individual tasks.

Implications for Venture Investors

The comparison between January and February suggests several structural dynamics shaping venture capital deployment in real estate technology.

First, a decline in transaction volume does not necessarily indicate reduced investor interest. Instead, it may reflect greater selectivity as investors prioritize companies with clear revenue models and strong market positioning.

Second, the presence of large growth rounds can significantly influence aggregate capital deployment even when overall deal activity moderates.

Finally, sector-level capital concentration suggests that investors continue to prioritize companies capable of operating across financial systems, infrastructure networks, and large property portfolios.

A More Selective but Still Active Venture Market

The first two months of 2026 illustrate a venture capital market that remains active but increasingly disciplined.

While January saw broader deal participation across early-stage startups, February’s dataset reflects a smaller number of transactions accompanied by several large growth financings.

For venture capital investors and institutional allocators, this pattern suggests a proptech ecosystem that is evolving toward greater capital concentration and stronger underwriting standards, while still supporting innovation across the global built environment.